To be held at GAAR offices on Thursday, October 2nd, 2014

Spreadsheet tools:

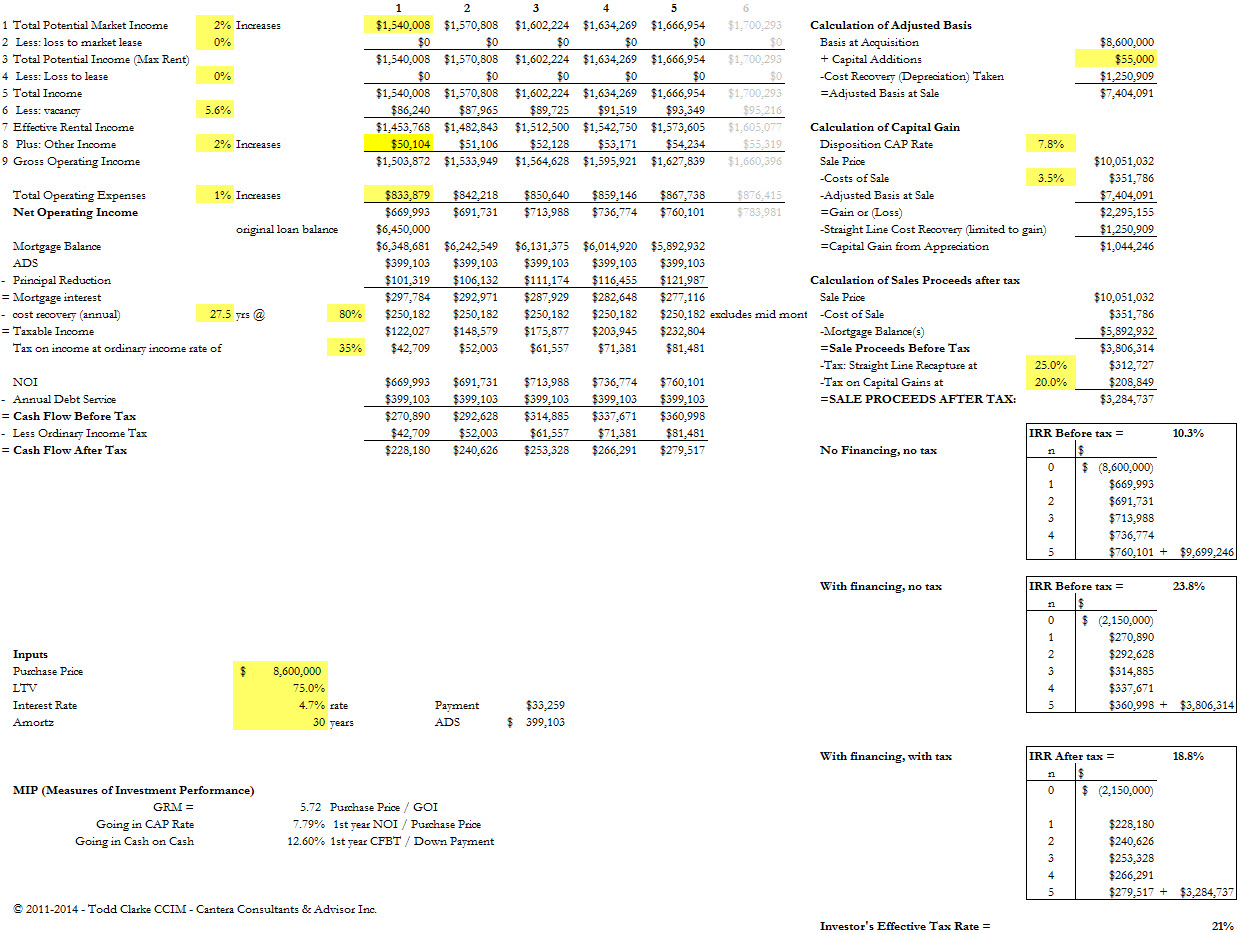

DTC-IRR-Model-v15-comm-blank-Citadelapartments

Confessions of a Commercial Real Estate Consultant

View Cantera Consultants & Advisors Inc. recent consulting assignments

To be held at GAAR offices on Thursday, October 2nd, 2014

Spreadsheet tools:

DTC-IRR-Model-v15-comm-blank-Citadelapartments

If you are feeling a bit rusty on measures of investment performance, the Investment Basics course will provide a sound foundation in the basic tools to analyze income producing real estate.

If you are feeling a bit rusty on measures of investment performance, the Investment Basics course will provide a sound foundation in the basic tools to analyze income producing real estate.

This hands on course includes simple to use spreadsheet tools to help you in analyzing investments using the basic measures of investment performance including:

– GRM

– Cap Rate

– Cash on cash

– IRR

and you will walk away with a sound understanding of the major investment benchmarks and tax benefits of owning real estate.

Both courses are hands on and its strongly encouraged that you bring your excel or numbers based laptop, tablet, smart device, etc.

Example of the financial analysis tool used in this course:

Register for this or any other course at www.canteraconsultants.com/cca2015 .

Additional information about your international award winning instructor can be found at www.toddclarke.com

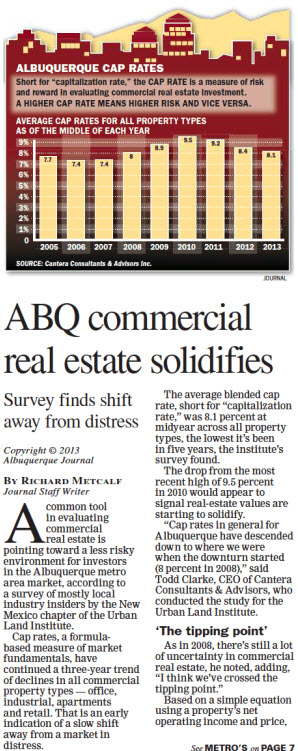

In in Albuquerque Journal article dated October 8th, 2013, Albuquerque was rated the 3rd best market in the country for rent growth.

The NM Chapter of the Urban Land Institute released its 2013 Commercial Real Estate and Value survey last week at the joint Apartment Association of NM and Urban Land Institute Market forum luncheon.

Previous value and cap rate surveys performed by Cantera Consultants & Advisors Inc. can be found here for 2011 and here for 2010.

Read the full article from the ABQ Journal here

Read the full article from the ABQ Journal here

The complete 11 x 17 version of the survey can be found by clicking here.

![]()

Yesterday’s Wall Street Journal reported that Susan Combs, Treasurer for the State of Texas is pushing for new legislation that would require local governments to add up their total debt obligations and disclose it to their constituents, the tax payer.

GREAT IDEA SUSAN!

Her office has also signed the light on Texas with a “Texas its your money” website that shares a ton of financial information about the states budgets.

New Mexican’s shouldn’t we demand the same?

Global Capital Markets> JLL Global Markets

Jones Lang Lassale – https://www.joneslanglasalle.com/Pages/Research.aspx

AND

most of them will be left behind by the top 50 cities in china

and Capital Flows –

![]()

Thanks to the Oregon Association of Realtors for hosting Views from the future of commercial real estate.””

PDFs of the presentations can be found here

Introduction – Todd Clarke CCIM – OAR-Intro-ViewsfromtheFrontier-10222012-v4

Office – Patricia Lynn CCIM NotesfromtheEdge Office-PatriciaLynn6c

Industrial – Sam Foster CCIM ViewsFromTheEdge-Industrial-SamFoster-v04302012-v2dtc

Residential/Multifamily – Todd Clarke CCIM – ViewsFromTheEdge-Residential-ToddClarke-v10252012-v6dtc

Latest and greatest apps – can be found here.

Confessions of a Commercial Real Estate consultant can be found here.

OAR-CCA-ConfessionsofaConsultant-10242012

The following is Todd Clarke’s excerpts from the Office of the future presentation – given first at NAR in 2012, with a Seattle update in 2013

The NM Mortgage Finance Authority’s annual housing seminar is coming up – 8/22-24/2012 – don’t wait to register!

A quick update to this posting (12/19/2011): This article about China’s property bust reminds me of a saying I learned during my travels in China “In my first month, everything in know about China would fill an encyclopedia. In my first year, everything I know about China would fill a book. In my first decade, everything I know about China would fill one page.”

I thought this email chain was a perfect example of being able to take CCIM 102 market analysis knowledge and apply it to global dynamics.

Fellow CCIM instructor Carl Russel wrote me the following email about a video on China he recently saw:

Haven’t we been teaching CCIM 102 in China for a number of years? Maybe they’re not as smart as we thought. If they have so much money, why don’t they invest in the United States….oh, they already are….never mind…Is this a 102 Case Study, or should it have been? Unbelievable video non youtube.

Carl G. Russell, CCIM, SIOR

Executive Vice President

George J. Smith & Son Realtors

and my response is below:

Carl-

Thanks for sharing – very interesting story – I am adding it to my ongoing list of resource on China Demographics for an article that I have been working on for quite a while now.

The whole idea of this much housing being empty is amazing.

If you have read Greg Lindsay (Skip @ CCIM’s son) book, Aerotropolis, he mentions that there are between 125 to 150 cities in China with a population over a million people compare that with 8 to 20 (depending on if you count “cities” or “MSA’s”) in the United States. Noted author, Greg Lindsay has dubbed many of these “instant cities“.

Many of these cities were created in the last 30 years as China has pulled over 350 million people out of rural poverty into urban jobs.

Since they don’t share their census info, and measuring is often erratic at best, many scholars have spent time trying to do simple things like determine trade areas in China like this report.

Today, there are more “urban” Chinese than there are American’s (total). There are more Chinese that speak English, than there are American’s (total). There are almost as many single men in China who have no hope of finding a wife (due to the gender imbalance from the one child policy which averages 119 boys for every 100 girls) as there are men in America.

I would disagree with the story about the lack of demand for these housing units, since a majority (just under a billion people) of China’s population is still considered rural, and unlike here, needs government approval to move into the large cities. As China continues its precarious balance between keeping the urban population happy with low food prices and the rural population with high food prices (this tight rope act has not prevented tens of thousands of “protests’ this year alone), it will be improving its agricultural efficiency, moving hundreds millions into the cities to pursue industrial (or information) employment, which will provide the income to pay for the housing.

Assuming 3 people per household, 64,000,000 empty apartments would support 192,000,000 people, or about 20% of the current rural population. Looking at it that way, I feel there is a similarity between these empty cities and America’s company towns of a hundred years ago – manufactures like Ford, Cannon, and many others created towns and filled them with their employees.

That said, I know many of us who have visited China on and off over the years have been amazed and appalled at the brutal efficiency central planning.

Lest anyone get their hackles up and try to turn this a political conversation, know that like them or not, the sheer scale of what they have achieved in 30 years is unprecedented in this planet’s history, and as much as we may bemoan lost manufacturing jobs to China, those jobs have pulled hundreds of millions out of severe poverty and their pay scale is rocketing upwards to the point where it is possible that the average Chinese person’s salary could match western European levels.

Finally, I liked the end of the video – watching the agents sell the reporter – it reminded me of GlenGarry / Glen Ross (the ABC’s – always be closing).

Thanks again for sharing!

Todd

Additional resources:

Urban vs. Rural

PRC demographics – http://en.wikipedia.org/wiki/Demographics_of_the_People’s_Republic_of_China

China demographics by sex

USA cities by population

USA housing breakdown –

http://ilookchina.net/2011/03/13/western-minds-may-have-it-wrong-about-china-building-empty-cities/

CCIM has just released the video interview with Greg Lindsay, author of Aerotropolis: The way we will live next from the CCIM Live 2011 conference held in Phoenix last month.

Earlier this year I wrote my review of this fabulous book which can be read here.

Greg’s powerpoint webinar from August 2011 is available at the CCIM website.

Cantera Consultants & Advisors has just released its 2011 value survey for NM Commercial Real Estate. The survey reflects the collective wisdom of industry professionals in NM.

Although Cantera uses the survey primarily for the benefit of it’s during property tax protest hearings, the survey has become staple in the commercial real estate market and is widely used and quoted by many of the brokerage, appraisal firms and county assessors in NM.

The most interesting trend reported in this year’s survey is the indication that most of the commercial property types have turned the corner on decreasing values as CAP rates have started to decrease (slightly).

Tomorrow’s edition of the Business Outlook in the Albuquerque Journal will highlight information from the report.

Last year’s survey results can be found here.

The 2011 value survey can be found CCA-Survey-10012011-v10.

Aerotropolis, the way we’ll live next

Authors: Greg Lindsay & John D. Kasarda,

Publishing Info: Farrar, Straus and Giroux, Nonfiction, First edition published March 1st, 2011

As an international instructor for the CCIM institute I discovered that the book, Aerotropolis: the way we’ll live next dovetails nicely with what the just-in-time delivery model as a primary driver of demand for industrial space that we teach in the CCIM 102 course, I would highly recommend it to anyone in commercial real estate.

As a rabid book consumer, I will easily digest about 100+ books a year, and without a doubt, Aerotroplis: the way we’ll live next has become not only my favorite book of this year, but one of my all time favorite business books. It is one of those rare books that I thoroughly enjoyed reading that I found myself moderating how much I could read daily so I can push the ending of the book out as long as possible.

My favorite magazine, The Economist recently offered a glowing review of Aereotroplis, stating “In Aerotropolis, John Kasarda of the University of North Carolina and his co-author, Greg Lindsay, convincingly put the airport at the centre of modern urban life.”

The theme of the book is that successful cities of the future will be wrapped around successful airports and those cities that can’t adapt may be passed by. Its authors state the books hypothesis as an equation related to time “The aerotropolis is a time machine. Time is the ultimately finite commodity setting the exchange rates for all the choices we make.”

Author and reporter, Greg Lindsay, expands and expounds on the John Kasarda’s original idea that airports are the highways of the future. As a former Fast Company and Wired magazine reporter, Mr. Lindsay racks up the frequent flyer miles talking with civic leaders, CEO’s and company logicians as he interviews them on their home turf about the importance of air transit to their communities, companies or supply chains future.

As a fellow traveler, I reminisced about Mr. Lindsay’s travels to well-known airports like Chicago’s O’Hare, Atlanta’s Hartsfield, Amsterdam’s Schiphol, or even Hong Kong’s International, but I was green with envy over his trips to Dubai’s Al Maktoum International Airport or South Korea’s Incheon airport and adjoining master planned Songdo International Business District. One story of Mr. Lindsay tracking his gift of flowers from the Aalsmeer flower auction in Amsterdam to his mother’s front porch will endear Mr. Lindsay to the reader as an extremely diligent reporter and respectful son. Even more surprising than his few thousand mile journey for flowers was his mother’s reaction.

Some of the books concepts in the book are eye opening such as “The world’s urban population is poised to nearly double by 2050, adding another three billion people to places like Chongqing. We will build more cities (and slums) in the next forty years than we did in the first nine thousand years of civilized existence. The United Nations predicts the vast majority will flood cities in Africa and Asia, especially China.”

Or this quote about South Korea “South Korea’s capital is the archetypal twentieth-century megacity, doubling in size every decade or so since 1950 to twenty-four million inhabitants—the second most populous on earth after greater Tokyo.”

Or my favorite quote about a Chinese based manufacturer: “We had barely crossed the border before he opened his laptop and began walking me through the true costs of those shipments. He’d built a widget calculating every conceivable variable: the weight, volume, value, and quantity of the products in question; the lead times for sourcing and building them; time spent in transit; their shelf life; the spread between paying his vendors and being paid himself; the cost of money in the meantime; and the cost of returns. An entire calculus, in other words, underlies the pivotal question of our era: What is the price of speed? The widget’s answer: slow is more expensive. The only thing faster than a FedEx 777 Freighter out of Hong Kong is the velocity of money, and the last thing Casey wants to pay for are the days his parcels are stuck on a boat. Obsolescence sets in the moment they leave the factory. “Revenue evaporation,” he calls it. “Air freight is key,” he muttered while running the numbers. “We like to work with products that can go by air. We build them in Shenzhen, and they’re in New York two days later. Time is often our number one currency, and the dollar is second.” ”

And this quote summarized the breath taking feelings I experienced in my many visits to China for CCIM’s education program: “China is placing the single biggest bet on aviation of any country, ever. Even before the crisis and China’s subsequent stimulus, the central government announced as part of its Eleventh Five-Year Plan that it would build a hundred new airports by 2020, at a cost of $62 billion. The first forty were ready last year. The vast majority lie inland, hugging provincial capitals and secondary cities bigger than any in the States. Full-scale aerotropoli are planned for China’s western hubs, Chongqing and Chengdu, and its ancient capital. Besides airports, China laid as many miles of high-speed railroad track in the last five years as Europe did in the last two decades. The trains, in turn, are meant to keep people off the highways, to which China’s adding thirty thousand miles—enough to eclipse the American interstate highway system. China’s planners have internalized the lessons of America’s Eisenhower-era infrastructure boom, designing a world-class system for moving people and goods quickly, cheaply, and reliably across any distance, whether locally by highway, regionally by rail, or globally by air. The plan is to pick up and move large swaths of the Delta hundreds or even thousands of miles inland. There is nothing to stop them.

And this quote on where the future global cities will be “Finding another five hundred million passengers 7should be easy. China has anywhere between 125 and 150 cities with populations greater than a million. The United States has nine; Europe, thirty-six. When the first phase of China’s airport-building boom is complete, the number of hubs handling thirty million passengers annually—more than Boston’s Logan or Washington’s Dulles—will have risen from three to thirteen, all of which will be the host of aerotropoli. By the time they’re finished in 2020, 82 percent of the population—1.5 billion people—will live within a ninety-minute drive of an airport, nearly twice the number today.”

The book dovetails nicely with some of my other favorite business reads like Marc Levinson’s “The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger” and Sasha Issenberg’s “The Sushi Economy: Globalization and the Making of a Modern Delicacy” both of which deal with just in time delivery and creating new markets.

Additional topics addressed in Aerotroplis include Peak Oil vs. Peak Food, globalization as a tool to pull the poor into the middle class vs. the carbon footprint of globalization via air travel, and the true cost of air travel in both economic and environmental terms.

If you enjoy Aerotroplis as much as I did, you might also read the June edition of Southwest Airline’s Spirit magazine as Mr. Lindsay has recently penned an article titled “Corporate Latter”. In this article he builds on the concepts discussed in Aerotroplis and discusses how technology has allowed us to shift away from being tied to an office, setting up shop at any location (http://www.spiritmag.com/click_this/article/the_corporate_latter/) . One economic development guru and author, Mark Lautman, is pushing this idea as the next evolution of cutting edge business recruitment – to scale down the benefits big corporations receive so communities can chase the highly mobile, quality of life comes first businessperson/consultant who eventually expands their business and hires staff. According to “When the Boomers Bail: A Community Economic Survival Guide”, this segment of our economic businesses is one of the fastest growing.

Not only would I highly recommend you read Aerotroplis, I would encourage you to purchase copies to share with your family, friends and clients as the conversations started from the concepts in the book are engaging, enlightening and very relevant to anyone with commercial real estate.

Todd Clarke CCIM

Aerotropolis can be purchased at: http://www.amazon.com/Aerotropolis-Way-Well-Live-Next/dp/0374100195/ref=sr_1_1?ie=UTF8&qid=1306590616&sr=8-1

Bob: what do you have for us today Todd

Todd: Good morning Bob! It’s hard to believe the holidays are already upon us and before you know it the end of the year will be here. As that time approaches, many of our customers wonder what 2011 will hold for the real estate industry and whether NM’s real estate market will lead, follow or diverge from national trends.

Bob: Todd, do you have a forecasting resource to help answer these question?

Todd: We sure do Bob, our firm has followed a publication called “the Emerging Trends in Real Estate” which is published by the Urban Land Institute and Price/Waterhouse/Coopers. For 32 years the authors of this publication have called upon the leading experts in the real estate industry to ask them what they see in their business in the coming year. This report provides an outlook on U.S. investment and development trends, real estate finance and capital markets, with a focus on key property sectors. The report draws on formal and informal surveys of real estate executives, investors, developers, and market experts around the U.S., including survey responses from over 500 real estate executives and personal interviews with over 125 industry leaders.

Bob: Sounds very comprehensive Todd, where can our listeners get a copy?

Todd: Bob there are two ways to get a copy – you can join the Urban Land Institute at www.uli.org, OR, you can attend their “Outlook NM” event to be held on the evening of December 9th, 2010

Bob: Can you tell me a bit more about this event?

Todd: I sure can – the national speaker is Chuck DiRocco from Price/Waterhouse/Cooper and he will be followed by our local panelists, Steve Maestas at Maestas Ward who will talk about retail, John Ranson of Grubb & Ellis who will address Office and Industrial, Jim Folkman of the HomeBuilders of Central NM who will discuss the single family residential market, and I will be covering the apartment industry.

Bob: Sounds like a full event – how can our listeners participate?

Todd: The cost of the event, which includes the publication is $60 – to RSVP – call the local Urban Land Institute office 505-269-7695 or call me anytime at 440-TODD.

Cantera Consultants & Advisors has just released the results from our latest valuation survey. This survey was performed over the summer of 2010 with real estate owners, investors, lenders, brokers and appraisers.

The attached document demonstrates the changes in CAP rates and values from 2005 to 2010.

Click here for the survey results and a related newspaper article CCA-Survey-07092010-v8plusJournalArticle

Posted in our sister blog, Todd Clarke’s Technology Corner, is an obituary of the man who developed the hardware for the first personal computer.

His fulltime job was as a scientist at Sandia National Labratories, but his interests were in developing computers that the public could use.

His company, MITS, developed the hardware, but he needed a software operating system to make the machine more accesible, and he and heard of a bright young programmer in the Seattle Area, Bill Gates, who might be able to write what he needed. Bill and his partner, Paul Allen worked around the clock from some down and out Route 66 motels to write the first operating system under their new corpoorate name, Microsoft.

This corporate photo, taken in 1978, shows the original Microsoft staff.

Thank you Dr. Edwards for cementing Albuquerque’s role in computer history.

The juxtaposition of news story about the economy are interesting – on one hand the Federal government has declared a victory on turning around the economy, on the other, those of us in the commercial real estate business know that until there is transparency in the lenders holdings, the loans will not flow, the capital markets will not return, and the transaction volume will remain virtually non-existent.

Good news from the Albuquerque Journal (need I say anymore?)

The not so good news about capital markets in the commercial real estate world, from yesterday’s RealShare conference titled Warning Signs.

The Wall Street Journal had a dour article on the ballooning balance of commercial backed securities.

President Truman once asked an economist his opinion –the economist replied with something like “on one hand it could be good, on the other hand it could be bad” to which Truman quipped “next time bring me a one handed economist”

Special thanks to fellow Realtor Ric Thom for sharing this:

This is an important message from Ric Thom, President Security Escrow Corporation, Albuquerque, New Mexico.

May 26, 2009

HR 1728: The Taking of Private Property Rights

Congress is trying to greatly restrict seller financing. This is a taking of our private property rights. The US House recently passed HR 1728 which limits you as an individual to sell real property using seller financing to only once every 36 months (HR 1728 Sec 101 Definition (3)(E)).

This bill was written to amend the Truth-In-Lending Act to regulate residential mortgage loan originators. This stems from the Secure and Fair Enforcement for Mortgage Licensing Act of 2008, or S.A.F.E, which established a national registry and standards for mortgage brokers. This is all directed at mortgage brokers, mortgage companies and banks. These are third parties that provide loan proceeds to the buyer to purchase property. That’s a good thing, but for some reason Congress has included private property owners who wish to sell their property using seller financing. Seller financing is where the buyer and seller negotiate a price, a payment plan, and interest rate. It’s an installment sale where the buyer pays the seller monthly and the buyer gets the use of the property. This is a frequently used method of buying and selling real estate especially in this economy of tight money. Banks are just not lending on, or are requiring huge amounts of cash down on, certain types of properties.

Seller financing is used tens of thousands of times every year, if not hundreds of thousands of times, to sell real estate. In New Mexico alone, with a population of fewer than 2,000,000, it is used over 5,000 times a year.

These acts are over-reaching and will have unintended consequences. The definition of a residential mortgage loan according to the Housing and Economic Recovery Act of 2008 means any loan primarily for personal, family or household use that is secured by a mortgage, deed of trust or other equivalent consensual security interest on a dwelling or on residential real estate upon which is constructed or is intended to be constructed a dwelling (Sec 1503 Definition (8)). This means any vacant land would fall under this act. A dwelling can be a house, condo, or mobile home. Here are just a few examples of the consequences:

• Let’s say you are about to lose your home and you need another $1000 a month to make ends meet. You decide to sell your five acres in the mountains and your 1982 single-wide mobile home on one acre by the lake to make your mortgage payment. Banks are not lending on these types of properties and you need a quick sale, so you use seller financing. The problem is you need to sell both to get an extra $1000 per month, but the government has prohibited you from doing so because of the one every 36 month rule.

• Suppose you have a self-directed IRA. Every year you buy property with cash out of the IRA. You then sell it using seller financing so you can get a 6% interest rate. You will be prohibited from doing so under the Act.

• Let’s say you have four rental houses that you own free and clear. Part of your retirement plan was to sell them using seller financing with a 6 to 7% interest rate and a 30 year amortization providing a nice, monthly income. You don’t want cash because CDs only pay 2% and you already lost money in the stock market. But, under this act you are prohibited from selling them now. You can only sell one every 36 months.

These scenarios go on and on. They are as unique as the individuals and the properties. Real estate is not just a house in a California suburb. It is also vacant land, non-conforming housing, land and mobile home, duplexes, triplexes, farms and ranches, and recreational properties. These types of properties would fall under the Act. Not everyone invests in the stock market. A lot of people invest in the above types of real estate. Not everyone wants to cash out when they sell their property; some people like seller financing for the income stream. Most states have escrow companies that hold the deeds or releases for buyers and sellers. They also keep track of the principal and interest and report interest to the IRS.

This bill takes away our right to use seller financing as we see fit. House Bill HR 1728 should exempt anyone who offers or negotiates terms of a real property sale financed in whole or in part by the seller and secured by the seller’s real property.

Why should individuals who had nothing to do with this crises be punished for the sins of the greedy Wall-Streeters? These acts are for mortgage machines, not Ma and Pa. I know the government is concerned about predatory practices, but is seems the local district attorney would be a more effective hammer than to regulate, restrict, and police every real property owner in America. Besides, seller financing is not lending. It is an installment sale. The seller has agreed to receive their equity over time, plus a negotiated interest rate.

House Bill HR 1728 is headed for the US Senate. Please write your senator and have them exclude seller financing from these acts that are supposed to regulate the previously unlicensed mortgage brokers. Write your state’s Realtor Association and the National Association of Realtors and ask them to help stop the government from taking away our right to sell our property the way we want to and when we want to. There should not be any restriction on how many properties we sell during a certain time period.

What’s next – just one transaction every 5 years, or no seller financing at all? This restriction is the last thing America needs in this great real estate compression. Please act now. Exempt Seller Financing From HR 1728. Please forward this to anyone you think should know about this issue.

To locate your Senator go to http://www.senate.gov/senators

To locate your state’s Realtor Association go to: http://www.realtor.org/leadrshp.nsf/webassoc?OpenView

For further information contact:

Ric Thom

President

Security Escrow Corporation

Albuquerque, NM

ricthom51@yahoo.com

(505)266-3487

Albuquerque Apartment market update2008 in review, looking forward to 2010 by Todd Clarke CCIM

The saying “may you live in interesting times” certainly seems to fit in today’s environment. Although the author and origin of this phrase is unknown, it is believed that it was composed as a curse and included two more phrases:

– May you come to the attention of those in authority

– May you find what you are looking for

Certainly, I think we could agree that our country’s financial sector is currently living under all three auspices.

In the following update, I attempt to summarize what is going on in today’s apartment market analyzing each of the components that the apartment market depends on for success, including a national perspective, and drilling down to our own local market.

Demand driver for apartment units

One of the fundamentals of the apartment industry is the concept that the occupancy of apartments is driven by population growth which is driven by job growth. By following job growth, one can make reasonable projections of future apartment occupancy.

National Employment

Between December 2007 and December 2009, unemployment increased by 2.3% to 7.2%, which means there are an additional 3,000,000 people without jobs. Unemployment has not been this high since 1992, and forecasts indicate this trends will likely continue as more and more companies are announcing layoffs.

Demand driver for apartment investors

The ability for an apartment investor to convert the equity in their property into cash depends on the liquidity of the financial markets, so financing is a major driver of buyer demand for apartment investments. When financing dries up the audience of future buyers becomes limited and, the investors risk rate increases as the safety of their net equity becomes less certain.

How did we get here?

Late in 2007, a perfect storm of excess liquidity, irrational exuberance, dubious rating assignments and quirky quant modeling (http://en.wikipedia.org/wiki/Quantitative_analyst ) assaulted investment markets in our country, and one by one, major banks, insurance companies, corporations, and now real estate investors are falling victim to the ensuing outcome.

As the economic trends continue to spread gloom and doom, comparisons are often made to depression era. I recently read John Kenneth Galbraith’s “The Great Crash of 1929” book which provides a detailed overview of that era. Certainly, some parallels exist between the two – the similarity of the downward spiral. The fact that both downturns were accelerated due to the great deal of leverage used for investments, limited cases of fraud, and the belief that the would continue to increase. The depression also was an unregulated free-for-all where numerous companies existed solely to invest in other companies, many of whom had only an idea and marginal cash flow or assets. Investors had limited information and bench marks to measure an investments return, except for its stock value. Today’s investor suffers from an overload of information and analysis, making it harder to sort out what is important and relevant versus the insignificant.

The largest difference between the 1930’s depression and today is three fold: improved transparency in market trades/information, increased sophistication of the market and increased oversight by our government.

Globally

From a macro perspective, part of the current economic crisis can be traced back to America’s ongoing trade deficit with countries like China. China in turn has reinvested our trade deficit dollars in USA government backed securities and treasury bills, effectively binding together the two countries economically even tighter. The national debt currently exceeds $10 trillion dollars (http://www.brillig.com/debt_clock/) and continues to increase at the rate of $3.31 billion a day since September of 2007.

China’s choice to reinvest those funds back into the United States, has increased the monetary supply, which has increased the access to capital for most investors. It created excess liquidity as there were more investors chasing few deals. As the market continued to climb to new heights, many investors started to believe in a “new methodology” for property values which only increased the disconnect between prices and the elementary market fundamentals. Said another way, as long as the market was increasing in value, more and more investors were willing to place their equity in any investment, with the hope of increasing prices, often ignoring the fact that the market was overdue for a correction, which historically purges the excesses of the market of equity and restore balance between the number of sellers and buyers of investments.

WTF? (where is the financing?)

On a Federal level, the government continues to encourage lenders to fund loans in the marketplace with carrots (bailouts), and sticks (threats of government takeover). Unfortunately the lack of liquidity in the marketplace will not be easily remedied with carrots or sticks, but only with trust.

The mortgage market has been cast as this decade’s financial villain, but the reality is that even though liar (no documentation) and ninja (no income, no job) loans did nothing to improve the industry’s reputation, only a small percentage of the market has actually defaulted on their loan.

The silent villain in this financial meltdown is also public policy or federal legislation. Although this legislation was intended to create more home ownership opportunities it did so by creating a new class of mortgages – subprime, named for the borrowers, who had less than ideal credit.

While the percentages of foreclosures for these mortgage products is higher than historical averages, there is something more toxic underlying these mortgages – known as CDO’s or collateralised-debt obligations. A recent article in the Economist does a fabulous job of describing these instruments and their undoing:

“Muddling the Mortgage

Yet the idea behind modeling got garbled when pools of mortgages were bundled up into collateralised-debt obligations (CDOs). The principle is simple enough. Imagine a waterfall of mortgage payments: the AAA investors at the top catch their share, the next in line take their share from what remains, and so on. At the bottom are the “equity investors” who get nothing if people default on their mortgage payments and the money runs out.Despite the theory, CDOs were hopeless, at least with hindsight (doesn’t that phrase come easily?). The cash flowing from mortgage payments into a single CDO had to filter up through several layers. Assets were bundled into a pool, securitised, stuffed into a CDO, bits of that plugged into the next CDO and so on and on. Each source of a CDO had interminable pages of its own documentation and conditions, and a typical CDO might receive income from several hundred sources. It was a lawyer’s paradise.

This baffling complexity could hardly be more different from an equity or an interest rate. It made CDOs impossible to model in anything but the most rudimentary way—all the more so because each one contained a unique combination of underlying assets. Each CDO would be sold on the basis of its own scenario, using central assumptions about the future of interest rates and defaults to “demonstrate” the payouts over, say, the next 30 years. This central scenario would then be “stress-tested” to show that the CDO was robust—though oddly the tests did not include a 20% fall in house prices.

This was modeling at its most feeble. Derivatives model an unknown price from today’s known market prices. By contrast, modeling from history is dangerous. There was no guarantee that the future would be like the past, if only because the American housing market had never before been buoyed up by a frenzy of CDOs. In any case, there are not enough past housing data to form a rich statistical picture of the market—especially if you decide not to include the 1930s nationwide fall in house prices in your sample.”

-the Economist, “In Plato’s Cave”, January 22nd, 2009

Essentially, the Wall Street gurus packaged together a large bundle of mortgages, which then they split into a various pieces, obtaining a rating for each piece, obtaining insurance for those pieces with ratings, then selling those insured/rated portions of the mortgage pool as low risk assets.

Although there are a multitude of problems that have emerged, the largest is the total disconnect between the property owner and the property loan. As you pay the loan on your house today, the interest portion may go to one CDO, the principal portion to another, and the payoff of the loan to yet another. That all may work so long as you can make your loan payments. But if you lose your job and you can’t make loan payments, then which CDO do you negotiate with to buy more time?

Let’s say you’re an institutional investor, pension fund, or bank who owns a lot of these CDO’s and you see an uptick in foreclosures – in fact a doubling from the historical average of 3.5% to 7%. You would like to work with the property owners, but you don’t actually own their mortgage, just a piece of it. To work with the owner would require several other institutions to agree to work with the owner, which is unlikely, so the property goes into foreclosure.

With more foreclosures than the quant modeling indicated would ever be likely, the market for more collateralized mortgages evaporates, and now there aren’t any buyers for the good or bad parts of your portfolio.

Meanwhile, back in the neighborhood, home buyers are waiting to see if they can get a better deal from a future foreclosure than an existing seller, so the housing market starts to see a large decrease in the volume of sales. Pretty soon, buyers of home are waiting on the fence to see if better deals are around the corner, and the market activity goes from cool to freezing.

Without sufficient market comparable sales of homes or mortgage pools, it becomes harder for sellers of homes or sellers of mortgage backed securities to value their existing portfolios.

The nail in the coffin for a complete downward spiral: poorly defined account regulations

The lending log jam is further hampered by auditors in the accounting industry who feel the obligation to hold corporations to a series of accounting standards like the “FAS-157-Mark to Market” (http://www.toddclarke.net/?p=318). This standard impacts how corporations “value” their holdings. The auditors biggest complaint is the portions of this standard that leave it to the auditor to determine a discount rate. To an auditor, interpretation equates to increased auditor liability which further encourages the auditor to use a more aggressive discount rate than the market would typically experience.

The CCIM Institute is working with our nation’s leaders to provide clarity on these regulations. To quote CCIM’s national president, Mac McClure:

“Under the rules, the accountant must use three levels to mark to market: level 1 active trading market, level 2 observable market data, and level 3 auditor discretion or discounted cash flow. Just like the commercial real estate appraisal business, level 1 would imply the auditor must find comparables which, in a market like today, are really non-existent. Level 2 represents observable market data which, in today’s market, we have very little or no trading of Commercial Mortgage Backed Securities. Level 3 is the use of Discounted Cash Flow Analysis which is what we taught the RTC, FDIC, GAO, and all the other government agencies in 1987-1990 to use. In practice, accountants want to be told which one of these to use or they want to be given the flexibility to use the one that fits the situation clearly. Under the current rules, accountants are having a real problem getting to level 3 because of the wording “auditor discretion.” In my discussion with the head of one of the largest accounting and audit firms in the United States today, he said the word “auditor discretion” is the kiss of death for discounted cash flow because no auditor will jump that hurdle. Instead, they would rather deeply discount the value of the asset because there are no comparables or market data that subject themselves to the potential scrutiny of an Enron-type investigation. However, if those two words were eliminated, they would be free to use any of the three methods to underwrite value.”

As an analogy, let’s say you own a 100 unit apartment in a good location, that possesses minimal deferred maintenance, with a solid history of stable cash flows, that you recently purchased for $5M. In the last year, only one other apartment in that size range has sold and it was a a beater, down and out, crime infested in the worst neighborhood in the city. Since many sellers don’t have to sell, they wait to do so, which deprives the market place of good comparable sales, leaving only the desperate to sell.

According to an auditor/accountant, the lack of market comparables would make the Level 1 standard of an “active market” ineligible, and as this sale was the only “observer able market data” Level 2 doesn’t apply, so that leaves Level 3, the discount rate as the only available value option. Remembering the fate of Arthur/Anderson, the auditor picks a large discount rate (say 20%). All of a sudden the “value” of your property is far less than what you paid, than what you would sell it for today (or any day), and far less than the property’s loan, so your lender triggers a clause in your loan that allows them to call the entire balance if a particular loan to value ratio is not maintained. Foreclosure ensues, followed by a fire sale of the property, and if enough of these properties sell in distress, they will establish a new lower market value, which then starts the whole downward spiral over again.

This example illustrates the difference of using an average and aggressive discount rate on the same fictional property’s cash flows:

Net value of the property at 12% IRR Net value of the property at 32% IRR

The table on the left indicates the return an investor would receive for a $500,000 down payment on a series of future cash flows and a disposition in year 5. This return is a reasonable 12%.

Lacking comparable sales, auditors might use a much higher discount rate, say 32%. On paper, the net value of the property has decreased by $248,464 or 50%.

This example demonstrates that even though the property’s cash flow remained unchanged, its dynamics where still in balance, and it was performing quite well, but a few misguided words of legislation put the property, and the investor’s equity into jeopardy.

While this is a dire prediction, it seems many economists, like Susan Hudson-Wilson of Property Portfolio & Research (www.toddclarke.com/press/PPR_National_Employment-012009) are forecasting scenarios that include 32% decreases in national apartment values between 2007-2010.

Trust and transparency is at the heart of all these issues

So what happens if you are a financial institution holding a pool of mortgages or a portion of mortgages that are “highly” rated and the cash flow is less than what you thought? How do you value the balance of your portfolio if the accounting standards are not clear? How do you make sane business decisions when the rest of the market is extremely volatile?

You don’t – instead you end up losing trust. You can’t trust the valuations for your own portfolios and investments. If you can no longer assign value to your own portfolio then how can you trust that other companies and banks can?

Trust is the lubrication that keeps market gears turning.

Most of our financial system is built on trust. Banks that used to loan each other money short term, often overnight, no longer do so because they aren’t sure what kind of financial condition the lender, or the borrower is in. So they start holding on to cash. They start hunkering down.

Our Federal Government realized this for a brief time last fall when they offered to let financial institutions sell their toxic debt to the taxpayers, to get a clean start. But the fallacy in doing so was that the government assumed every institutions knew bad debt from good debt – and as we’ve already discussed, once the auditors apply a steep discount rate to all of your investments, bad and good start to look alike.

Transparency follows trust or as President Reagan was once quoted saying “Trust but verify”. During 2008, financial intuitions wrote down large portions of their portfolios value, but they couldn’t explain to their stock holders how they arrived at those write downs, and quarter after quarter, more and more write downs followed, to the point that stock holders no longer understood what they owned either.

To stop a run on the banks, the Federal Government created the Troubled Assets Relief Program (TARP). An impressive amount of federal money was set aside to become a safety net for the banks and their toxic debts. It has been more than three months since TARP was passed, and I think many people are starting to realize that what the banks truly needed is a safety net. A tarp covers your assets during a storm but this TARP has become an opportunity for the government to intrude into the day to day operations of a company on issues like the executive compensation and company sales junkets. It’s a bit like reshuffling the chairs on the Titanic right after it hit the iceberg.

It has been recently reported that there are a number of local and regional banks that opted out of the ability to tap into the TARP funds due to the uncertainty associated with the strings that the government is imposing on TARP recipients.

Keep in mind, part of this mess was created by social tinkering by our government and the thought that more tinkering, or taking on more debt will solve this problem appears counter intuitive to the solutions the market and this country need.

So what can the Federal Government do?

One economist indicated the best thing the government could do to expedite a cleanup of this financial mess would be to mandate all federally insured institutions replace their top management by a certain date, or risk losing FDIC insurance. As the new officers came on board, they would be extremely diligent in finding all of their toxic debt, and shedding it as part of their turn around process.

Lacking that, a second financial market could be created without the regulatory shortcomings of the current market. This new market should have clear accounting rules and more importantly, one regulator to report to.

In short, until transparency in the bank holdings is created, ideally with sound valuation methodologies, trust will not exist between the players which will only prolong the capital market crisis.

Translating the residential real estate market to the commercial real estate market

If residential mortgages provided the fuel for the CDO’s spark that led to the fire of the current meltdown, how has this spread to other markets?

For the most part, commercial real estate and apartments continue to have sound fundamentals, but many of these properties have loans that are payable in full in the next couple of years. One of the world’s largest industrial investors, ProLogis, has billions of dollars of loans that renew on stabilized, class A, industrial properties in the next couple of years.

The shift from excess liquidity to scarcity of finance has put these investors in a tenuous position leaving them with the options of waiting it out, hoping liquidity is restored, or wholesaling their assets to use pent up equity to retire existing debt.

This has recently been evidenced by the thrashing of stock values experienced by Real Estate Investment Trusts like ProLogis, AIMCO, UDR, and General Growth. Most of which have started liquidating parts of their portfolio (http://www.toddclarke.net/?p=211).

And now, your local perspective

During 2008, Albuquerque felt like it lived in a parallel universe that was disconnected from the national economy – jobs continued to roll in, foreclosures were some of the lowest in the country, single family housing held on to most of its values, apartment occupancies continued to increase, as so did rental rates.

Albuquerque Employment Overview

The ongoing gloom and doom on a national level is starting to permeate the Albuquerque economy as the capital crunch continues to starve many businesses of the funding they need for day to day operations.

As you may know, Albuquerque was recently rated one of the top 5 cities in the country to build wealth in. Although the ups and downs of Eclipse Aviation’s bankruptcy have garnered major headlines, the labor department’s (http://www.dws.state.nm.us/dws-Mnews.html) latest release of employment data indicates that unemployment has been creeping up slowly since last summer’s announcement that it was at a 30 year low.

Albuquerque Sales last year

2008 was not a banner year for apartment sales in Albuquerque. The volume of sales decreased by 75% from $336M to $82M, with the 100+ unit apartments leading the way decreasing in sales from $277M to $37M. In fact, further analysis of the 100+ unit sales indicates that both sales that occurred in 2008, were actually put under contract in 2007. While the overall volume of sales decreased, valuation benchmarks showed only marginal decreases ranging from 10% to 15%.

This graph shows the percentage of the total apartment inventory that sold year by year.

Break down by segment

Albuquerque is unique in that it has such an abundant supply of small and medium sized units allowing the small property investors to work their way up the investment ladder over time – conceivably making it possible today’s fourplexes investor to own a 100+ unit property in twenty years. As that investor moves up the apartment investment ladder to larger properties, they are able to support on-site management staff, 3rd party management, and increasing sophistication in property operations.

NM Apartment Advisors has broken down the classification of apartment investments into physical category descriptions that reflect the typical investor for that size range. Each of these investors has a different approach to value and desired yield.

Distressed Sales

For the first time in a long time, distressed sales are starting to have an impact in the average value of New Mexico apartment sales. NM Apartment Advisors classifies a sale that is listed as “short”, “foreclosure”, “fire” or “handyman special” as a distressed sale. In typical years, the number of distressed sales has a marginal impact on the overall marketplace, but in 2008, some 18.4% of the sales that occurred were sales under distress, which skewed market values even more than expected. For that reason, for those segments of the marketplace that experienced distressed sales (mostly apartments containing 8 units or less), two categories of the 2008 summary have been provided, one has all sales, and the other that only reflects the non-distressed sales.

The following is a summary of each of these segments of the marketplace:

100+ units: in total, the 100+ unit apartments makes up over 60% of the total number of units, but only 4% of the total number of apartment communities. During 2005-2007 buyers binged by buying up some 20% of the marketplace. Although two sales in this size range occurred in 2008, both were marketed and under contract in 2007, effectively making 2008 a year with no sales in this catergory.

*the “% sold of ABQ/RR” heading above represents the market churn, or the percentage of the marketplace that sold that year

NM Apartment Advisors Inc. took a property to market in this category in 2008, and was able to secure 18 offers from qualified buyers, but increasing volatility in the capital markets made securing financing all but impossible.

In summary, while buyer interest remains strong, buyers are limited today by lack of financing choices. In 2009, the deals most likely to close will be delivered to a purchaser with attractive assumable financing, or seller financing.

50to99 units: This segment of the marketplace makes up a small portion of the total inventory, and it is common to see very few transactions annually in this size range. For example, the only sale in 2007 was a 50 unit property that was sold to a condo converter. If we consider that sale to be an anomaly, then between 2006 to 2008, values on a price per unit increased 16%.

20to49 units: Like the 50 to 99 unit category, this portion of the marketplace is relatively small, but even it experienced a decrease in the total dollar volume of sales by 52%. CAP rates rose from 7.7% to 8.1% and the price per unit decreased 9% from its high in 2007.

5to19 units: While the overall volume of sales in this category decreased, the price per unit increased by 13%.

Fourplexes: although the fourplex marketplace only contains 9% of the marketplace in total number of units, they contain 35% of the total number of apartment communities. From 2007 to 2008, fourplexes experienced a decrease in sales volume of 64%, and a decrease in price per unit of 21%. 18% of all fourplex sales in 2008 were distressed sales, and even if those sales are excluded, the price per unit still decreased 14%.

Duplexes/Triplexes: Typically the units in this category often sell to owner/occupants who are more interested in the ability to live in the property than in its investment potential. Like the housing market, value decreases in this category are minimal. Adjusting for the 80% of the sales that were not distressed, the price per unit decreased by only 5%.

The impact of competitive investments in other markets

Although our office continues to receive phone calls from investors looking to expand their existing Albuquerque portfolio, many of them are chasing deals in markets that suffer from higher volatility like Phoenix, Las Vegas, the inland empire, and the Bay area which offer higher returns.

Local Financing

As dour as the financial news sounds, there are many local lenders in New Mexico who are continuing to loan on apartments. They’ve indicated that it’s back to the basics, sound property, sound borrower, sound underwriting, and for now, the lender is calling the shots on timing. Unfortunately, many of these lenders are capping their maximum loan at $20M.

To summarize

While Albuquerque’s internal economy is outperforming the national economy, the extended recession nationally is starting to take its toll locally and this could continue for a while. While many apartment values remain reasonably close to their recent high prices, an extended credit freeze could force more investors to liquidate at substantially discounted prices.

Our recommendation is simple – if your property has a loan that is good through 2012, and if you’re otherwise pleased with your property – we recommend you hold on to it until the national economy regains some sanity. If your property has a loan coming due in the next couple of years, we would highly recommend you begin working on refinancing that loan today, or worst case, realize that you may need to sell the property at a discount from the higher values the market experienced in 2006-2007.

The future going forward

Personally, I remain optimistic about the Albuquerque apartment market and I look forward to adding to our family’s portfolio with some of the opportunities that may arise this year.

And unlike the last major downturn, there is a lot of money waiting on the side lines, and a sense of optimism.

Rents/OccupancyStill to come – NM Apartment Advisors is currently updating its rent and occupancy survey, and upon completion, we will forward the results to you.

As always, I look forward to hearing from you about your property and your experiences during these interesting times.

Still here in New Mexico plugging away,

Todd Clarke CCIM

The above analysis is merely the opinion of a 20 year veteran in the commercial real estate sector, and it is based on the current market information, news stories, and anecdotal evidence as collected by its author, Todd Clarke. Additional analysis can be found on his commercial real estate blog, www.toddclarke.com.

I received this earlier last week from our good friend, Mac Maclure with an update on the how the definition of a phrase could be having a large impact on the current liquidation crisis:

I received this earlier last week from our good friend, Mac Maclure with an update on the how the definition of a phrase could be having a large impact on the current liquidation crisis:

Dear Members of the Faculty:

During this historic week in America as we experience another peaceful transition of power in our nation’s Capitol, your CCIM Management Team is approaching 2009 with a new outlook, new resolutions, and a fair amount of cautious optimism. While we have watched Wall Street and auto industry executives go before the U.S. Congress asking for bailouts, the commercial real estate industry continues to suffer from its own crisis. A vital CCIM member benefit is the Institute’s role as a legislative advocate for the commercial real estate industry. Through our affiliation with NAR and our partnership with IREM, we are part of a team that constantly monitors legislative and regulatory developments to shape the direction of today’s policy issues. In that role, the Institute must offer not only opinions but solutions to the current economic environment. This email addresses our approach to solving a number of the economic issues. While I recognize it is lengthy, I feel it is important that each of you have detailed information.

Chief Executive Officer Jonathan Salk and I went to Washington, D.C., in December to attend the NAR economic stimulus work group, which included representatives from various commercial real estate organizations. Prior to this meeting, the CCIM and IREM legislative committees were asked what a second economic stimulus package should include to stabilize commercial real estate markets. Both of our organizations felt that based on our member’s input, our legislative staff should develop a list of eight solutions, which are attached, that supported our stimulus provisions recommendations. The full Financial Crisis Background Paper is also attached. As a result, the NAR economic work group adopted six of the solutions as its platform, which are summarized in the attached Economic Stimulus Proposal.

However, as we all know the real benefit of our organization is the ability of our members to interact with Congress one on one in the district that elects them. For years our strength has always been in our grass roots involvement on a day to day basis. Therefore, I would like to give you a personal briefing of one of the major issues in our solutions fact sheet that should be addressed with each Congressman on a one on one basis by our members. The issue is called “Mark to Market” rules that were enacted after Enron in an attempt to eliminate potential problems in the accounting industry. Many people are running around Washington talking about “Mark to Market”, but few of them actually understand what they are talking about. Therefore, as Paul Harvey used to say, here is the rest of the story.

The Financial Accounting Standards Board has enacted a rule forwarded to the Securities and Exchange Commission called “FAS157 – Mark to Market”, which is used to determine the fair value for all CMBS programs as well as commercial real estate properties that are held in publicly traded vehicles. Each year under Federal Guidelines, auditors have got to, by Federal law, mark all publicly traded vehicles to market. Under the rules that the auditors work with, “FAS 157” fair value says the auditor must mark to market the new value of the asset every year on the balance sheet of the companies. Under the rules, the accountant must use three levels to mark to market: level 1 active trading market, level 2 observable market data, and level 3 auditor discretion or discounted cash flow. Just like the commercial real estate appraisal business, level 1 would imply the auditor must find comparables which, in a market like today, are really non-existent. Level 2 represents observable market data which, in today’s market, we have very little or no trading of Commercial Mortgage Backed Securities. Level 3 is the use of Discounted Cash Flow Analysis which is what we taught the RTC, FDIC, GAO, and all the other government agencies in 1987-1900 to use. In practice, accountants want to be told which one of these to use or they want to be given the flexibility to use the one that fits the situation clearly. Under the current rules, accountants are having a real problem getting to level 3 because of the wording “auditor discretion.” In my discussion with the head of one of the largest accounting and audit firms in the United States today, he said the word “auditor discretion” is the kiss of death for discounted cash flow because no auditor will jump that hurdle. Instead, they would rather deeply discount the value of the asset because there are no comparables or market data that subject themselves to the potential scrutiny of an Enron-type investigation. However, if those two words were eliminated, they would be free to use any of the three methods to underwrite value.

On January 13, NAR President Charles McMillan delivered testimony before the House of Representatives’ Committee on Financial Services and communicated these positions. Also on the 13th, the CCIM Institute cosigned letters, which are attached, to Representative Barney Frank and Senator Chris Dodd, that support a commercial-focused lending facility. Congressman Frank, chair of the U.S. House Committee on Financial Services, has introduced H.R. 384, which supports stabilizing and providing liquidity to the credit markets, including mortgage-backed securities.

This is just the start of this issue in Congress and we will be pursuing other opportunities with NAR and other coalition partners. We will also be flexible to consider issues that may not be part of our stimulus proposal. These difficult times present an opportunity for CCIMs to make our collective voice heard in the new administration. Join us on April 22 in Washington, D.C. for our annual Capitol Hill Visit Day and meet with your members of Congress. Go to http://www.ccim.com/members/govaffairs/capitol_hill.html for details and to register. As always, the CCIM Institute is very focused on advocacy efforts on behalf of this industry, and we need and appreciate your help to reinforce these messages with your own elected representatives.

If you have any questions or would like additional information regarding these efforts, please contact CCIM’s legislative staff at legislative_affairs@ccim.com.

Mac

Charles A. McClure, CCIM, CRE

2009 President – CCIM Institute

Chairman – McClure Partners

P.O. Box 802047

Dallas, Texas 75380-2047

972-663-3738 Office

214-384-9862 Mobile

mmcclure@mcclureusa.com

As major retailers like CompUsa, Mervyn’s, Linens and Things, Circuit City, fold one after another, leaving vacant spaces in major malls across the country, occupancy rates continue a downward trend, which eventually leads to decreasing rents and values.

Real Estate investors with the most leverage (i.e. the least amount of their own money), will be the hardest hit, but even lower leverage institutions are taking a hammering in their overall valuations.

What’s going on?

It has to do more with the capital markets than the dynamics of the real estate economy. According to a recent Wall Street Journal article, over $530 Billion dollars of loans are coming due in the next 3 years, including $160 Billion in 2009. Real Estate investors that counted on excess liquidity (or even some liquidity) in the marketplace, are now seeing their valuations hammered as the stock market’s perception is that many of these companies will be unwilling to renew their financing.

Some of this country’s largest owners, are

Real Estate Investment Trusts, or REIT’s are a special type of corporation (that is not double taxed) which allows passive investors to hedge their risk by investing in a large number of markets around the country (thus avoiding having all of their eggs stuck in one city).

As an indication of where Wall Street pessimism in the marketplace, take a look at the stock value of some of the largest and most well known REITS:

Equity Residential

A Co-Star article indicates that REIT’s values have seen decreases of more than 40% and that many of them are likely to run into a liquidity crisis.

It certainly is an interesting time to be in the business – the recent meltdown of the subprime crisis had led to a crisis of trust between lender’s – so much so that the SEC was recently quoted as saying

“The trust and confidence that counterparties require in one another in order to lend, trade, or engage in similar risk-based transactions evaporated to varying degrees for each firm very quickly. What would have been more than sufficient in previous stressful periods was insufficient in more extreme times.”

From a bystander’s viewpoint, it has been interesting to witness the country’s politicians mickey mouse with the free market, then run from the issues, then hold hearings to find blame, and now they believe they can solve it?

Unfortunately, they’ve avoided discussing the root causes of the capital crisis – public policy initiatives to get every American into a home (whether they could afford it or not), government interference in the free market by offering home ownership preferential tax treatment, and a lack of oversight when Wall Street started going bezerk creating complex financial instruments that neither them, the rating agencies, the buyers or the sellers understood.

The original plan for Troubled Assets Relief Program T.A.R.P was to allow lender’s to clear their slate clean of these bad debts, thus opening the market for future financing.

And guess what?

We still don’t understand them, and until we do, no one knows who has the hot potatoes (the bad debts), and until due-diligence is done to uncover those assets, those same lender’s don’t know what to convey to T.A.R.P. and their assets remain frozen as there isn’t market to buy and convey what you can’t quantify.

Unfortunately, the market doesn’t wait for solutions, it just keeps rolling, and its rolling off the precipice if the real estate investors and developers can’t renew their loans on existing, performing, assets.

Right now, solutions are most likely to come from the following arenas:

1. The capital markets start to thaw and we see financing return to the marketplace

2. a seperate financing vehicle is created, possibly under the T.A.R.P. program

3. Lender’s convert their debt positions into equity (which would require government approval).

4. The property owners start to liquidate other holdings (Prologis just announced a large sale of their Asian holdings

Until then? Look for continue decreases in real estate equity and the possibility that the canary may die, before one of these solutions are expedited.